One Big Beautiful Bill Act (OB3) Financial Aid Update

One Big Beautiful Bill Act (OB3) Financial Aid Update

Public Law 119-21, signed into law by the President in July 2025, goes by many names:

Working Families Tax Cuts Act, or One Big Beautiful Bill Act, or OBBBA, or OB3.

Regardless, the bill introduces sweeping changes into the finacial aid world which

largely go into effect July 1, 2026.

- Most changes apply to new student borrowers of Federal Direct Loans and their Parent Plus borrowers (undergrad students).

- Changes also apply to students enrolled at a less than full-time status (all students).

- Incoming freshmen and new transfer students who begin attending after June 30, 2026, and receive or borrow federal student aid, are fully under the new program policies.

- Legacy provisions will allow many returning students (and parent borrowers) to complete their degrees under previous program limits and policies.

Below is an overview of major changes and an examination of the impact to students and families by student type.

Incoming Fall 2026 freshmen and transfer students will fall completely under the new

federal policy.

Returning undergraduate students who have never borrowed federal loans and borrow

for the first time in 2026/27 will also fall under these new limits.

Loans

- Incoming and transfer students will adhere to the new Federal Direct Loan limits as shown in the table below.

Federal Direct Loan Borrowing Limits for Undergraduate Students

| Dependent Students | Independent Students | |

|---|---|---|

| (Except students whose parents are unable to obtain PLUS Loans) | (And dependent undergraduate students whose parents are unable to obtain PLUS Loans) | |

| First-Year Undergraduate Annual Loan Limit: |

$5,500 No more than $3,500 of this amount may be in subsidized loans. |

$9,500 No more than $3,500 of this amount may be in subsidized loans. |

| Second-Year Undergraduate Annual Loan Limit: |

$6,500 No more than $4,500 of this amount may be in subsidized loans. |

$10,500 No more than $4,500 of this amount may be in subsidized loans. |

| Third Year and Beyond Undergraduate Annual Loan Limit: |

$7,500 No more than $5,500 of this amount may be in subsidized loans. |

$12,500 No more than $5,500 of this amount may be in subsidized loans. |

| Aggregate Limit | ||

| Subsidized and Unsubsidized Aggregate Loan Limit: |

$31,000 No more than $23,000 of this amount may be in subsidized loans. |

$57,500 No more than $23,000 of this amount may be in subsidized loans. |

| Lifetime Limit*: | $257,500 | $257,500 |

*Lifetime limit, excludes Parent PLUS

Schedule of Reduction for Loans

- Beginning the 2026-2027 academic year, all unsubsidized and subsidized annual loan

amounts will be reduced based on enrollment status for those less than full time.

- Reduced Annual Loan Limit Percentage = (Number of Credit Hours Enrolled for the Term) X 100

(Number of Credit Hours Considered Full Time

for that Term for the Program of Study)

For a regular full-time example: a dependent freshman student enrolled in 12 credit hours for fall and spring will be able to borrow $2,750 each semester (100%).

For a part-time example, a dependent freshman student enrolled in 6 credit hours for fall and spring, which is 50% of full-time hours, will only be able to borrow up to 50% of the loan limit per semester, or $1,375. - Dropping a course during a term that drops you below full-time may affect your next term aid. If you are considering dropping a course, contact your financial aid counselor to see how your future aid may be affected.

- Reduced Annual Loan Limit Percentage = (Number of Credit Hours Enrolled for the Term) X 100

Pell

Students may be ineligible for a Pell Grant if the full cost of attendance is covered with non-federal grants and scholarships or if the student’s Student Aid Index (SAI) is greater than twice the maximum Pell Grant.

Students who have attended in the 2025/26 and previously borrowed federal direct loans will likely fall under what is called "legacy provisions."

Legacy Provisions allow current students or parents to temporarily continue to borrow under the prior federal loan rules and loan limits. Legacy eligibility is determined by federal law and is automatically applied if a student qualifies. You cannot opt out of a legacy provision in favor of new loan borrowing limits. It cannot be waived or declined.

- To qualify, a student must

- have a Federal Direct Loan disbursed on or before June 30, 2026.

- remain in the same program at the same school though undergraduates may change majors as long as they remain at the undergraduate level.

- not withdraw or take a break in enrollment.

- For semester students, the summer term is not compulsory. However, if you withdraw from the summer term, it will be considered a drop in enrollment which does result in a loss of the legacy provisions.

- The student must be within their expected time to complete the program (the shorter of three (3) academic years or the remaining program length).

- For example, a junior in the 2026/27 aid year, who has completed 2 academic years, has 2 years left in the legacy provision.

Schedule of Reduction for Loans

- Beginning the 2026-2027 academic year, all unsubsidized and subsidized annual loan

amounts will be reduced based on enrollment status for those less than full time.

-

Reduced Annual Loan Limit Percentage = (Number of Credit Hours Enrolled for the Term) X 100

(Number of Credit Hours Considered Full Time

for that Term for the Program of Study)

For a regular full-time example: a dependent freshman student enrolled in 12 credit hours for fall and spring will be able to borrow $2,750 each semester (100%).

For a part-time example, a dependent freshman student enrolled in 6 credit hours for fall and spring, which is 50% of full-time hours, will only be able to borrow up to 50% of the loan limit per semester, or $1,375. -

Dropping a course during a term that drops you below full-time may affect your next term aid. If you are considering dropping a course, contact your financial aid counselor to see how your future aid may be affected.

-

If you do not qualify for the legacy provisions, please see the Incoming Freshmen/Transfer Undergraduate Students section for more information about the changes to federal financial aid.

Returning students who have borrowed loans before

Parents have a limited exception to borrow under past Parent Plus loan limits which

is Cost of Attendance less Other Financial Aid + Scholarships. As always, parents

may select either a specific loan amount or mark "maximum loan" on the Parent Plus

loan application at www.studentaid.gov.

New students or transfers, OR returning students who are borrowing loan aid for the

first time in 2026/27

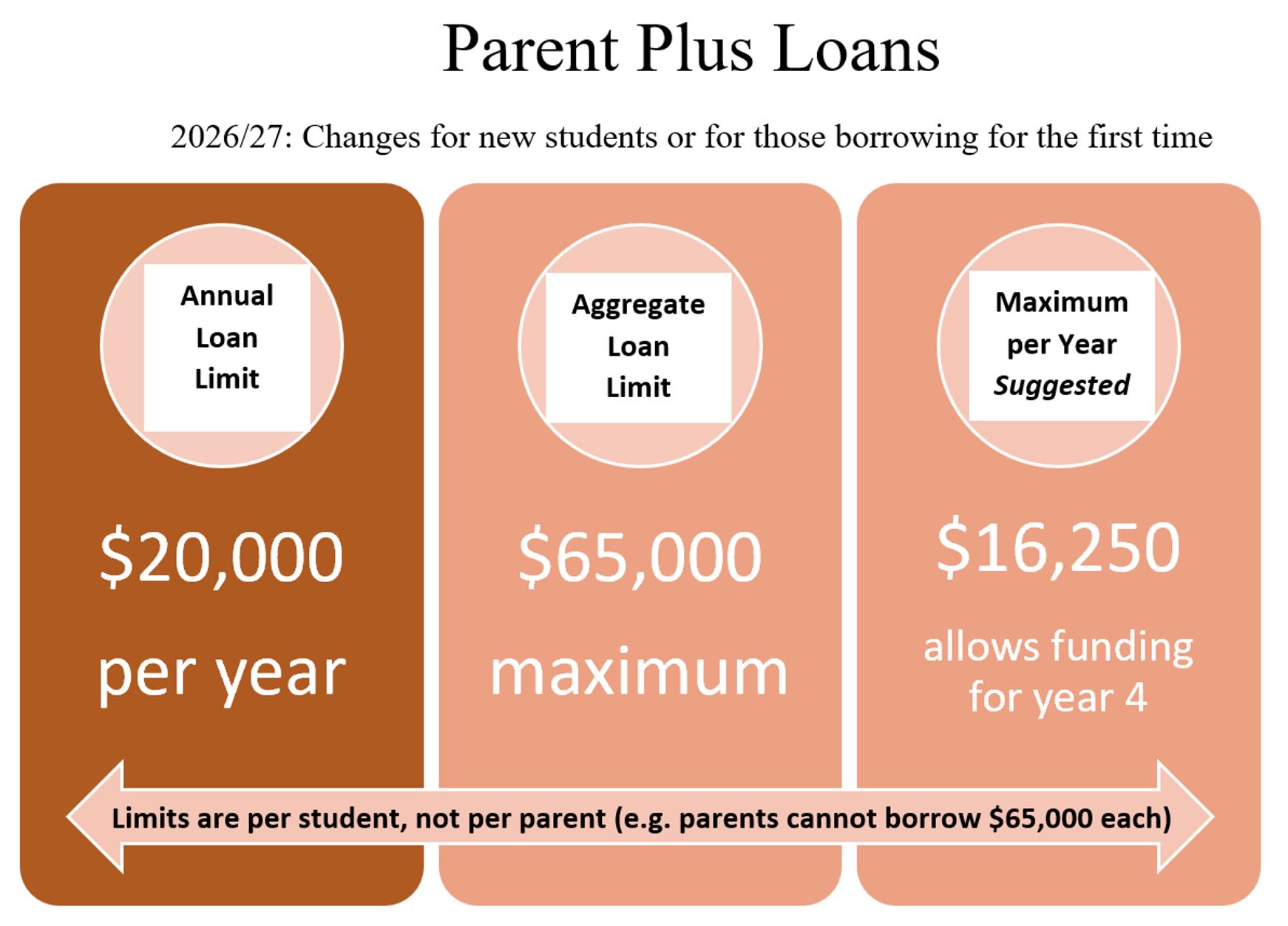

Parents may borrow up to $20,000 per year per student, with a lifetime limit of $65,000

per child.

- Note: this means if a parent borrows $20,000 for three years, only $5,000 of borrowing

will be left for year four.

- Parents may want to consider borrowing at $16,250/year maximum to even split the

$65,000 limit over four years.

Limits are student-based, so each parent may not borrow the $65,000 for the same student. It is $65,000 total per student between

either or both parents.

Incoming Fall 2026 graduate degree students will fall completely under the new policy.

MDiv students see "Professional Students" below.

Loans:

- The Graduate PLUS loan is no longer available.

- The new unsubsidized loan limit is $20,500 annually with a program limit of $100,000.

- The program limit does not include undergraduate loans.

- The lifetime federal loan limit is $257,500 which does not include undergraduate Parent PLUS loans.

Schedule of Reduction for Loans:

- Beginning the 2026-2027 academic year, all unsubsidized annual loan amounts will be reduced based on enrollment status for those less than full time.

- Reduced Annual Loan Limit Percentage is (Number of Credit Hours Enrolled for the Term) X100

(Number of Credit Hours Considered Full Time

for that Term for the Program of Study)

- Federal Direct loans will be reduced based on enrollment intensity.

- For a full-time example, a graduate student enrolled full time, or 9 credit hours,

will be able to borrow $10,250 per semester. - For a part-time example, a graduate student enrolled in 6 credit hours, which is 67%

of full-time hours,

will only be able to borrow 67% of the loan limit for the semester, or $6,868 each semester. Though, a student who attends 6 credits for fall, spring, and summer (total of 18 credits for the year) may borrow in thirds about $6833 per term, or $20,500 for the aid year.

- For a full-time example, a graduate student enrolled full time, or 9 credit hours,

Many students currently enrolled in Spring and Summer 2026, who have previously borrowed Federal Direct loans, will fall under the legacy provisions.

- Legacy Provisions: Allows for continuing students to temporarily continue to borrow under the prior federal loan rules. This means that students who qualify for legacy provisions may continue using Graduate PLUS loans and the prior federal loan limits.

- Legacy eligibility is determined by federal law and is automatically applied if a student qualifies. It cannot be waived or declined.

- Legacy Provision Qualifications:

- A Federal Direct Loan is disbursed on or before June 30, 2026.

- The student must remain in the same program at the same school.

- There is no withdrawal or break in enrollment.

- For semester students, the summer term is not mandatory. But if you attend summer and withdraw, it will be considered a drop in enrollment. This will result in a loss of the legacy provisions.

- The student must be within their expected time to complete the program (the shorter of three academic years or the remaining program length).

- Schedule of Reduction for Loans: Beginning the 2026-2027 academic year, all unsubsidized

annual loan amounts will be reduced based on enrollment status for those less than

full time.

- Reduced Annual Loan Limit Percentage = (Number of Credit Hours Enrolled for the Term/Number of Credit Hours Considered Full Time for that Term for the Program of Study) X 100

- Federal Direct loans will be reduced based on enrollment intensity. For a full-time example, a graduate student enrolled full time, or 9 credit hours, will be able to borrow $10,250 per semester. For a part-time example, a graduate student enrolled in 6 credit hours, which is 67% of full-time hours, will only be able to borrow 67% of the loan limit for the semester, or $6,868 each semester.

- If you do not qualify for the legacy provisions, please see the Incoming Graduate section for more information about the changes to federal financial aid.

Incoming Fall 2026 Professional degree students will fall completely under the new

policy.

Professional degree (as defined by the Department of Education) offered at the University

of Dallas is only the MDiv degree.

Loans

Graduate PLUS loans are no longer available to new borrowers.

The new annual loan limit for professional students is $50,000 a year with a program

limit of $200,000 which does not include undergraduate loans.

The lifetime federal loan limit is $257,500, which does not include undergraduate

Parent PLUS loans.

Schedule of Reduction for Loans

Beginning the 2026-2027 academic year, all unsubsidized annual loan amounts will be

reduced based on enrollment status for those less than full time.